.svg "page-1 (3)")

.svg)

.svg)

.svg)

.svg)

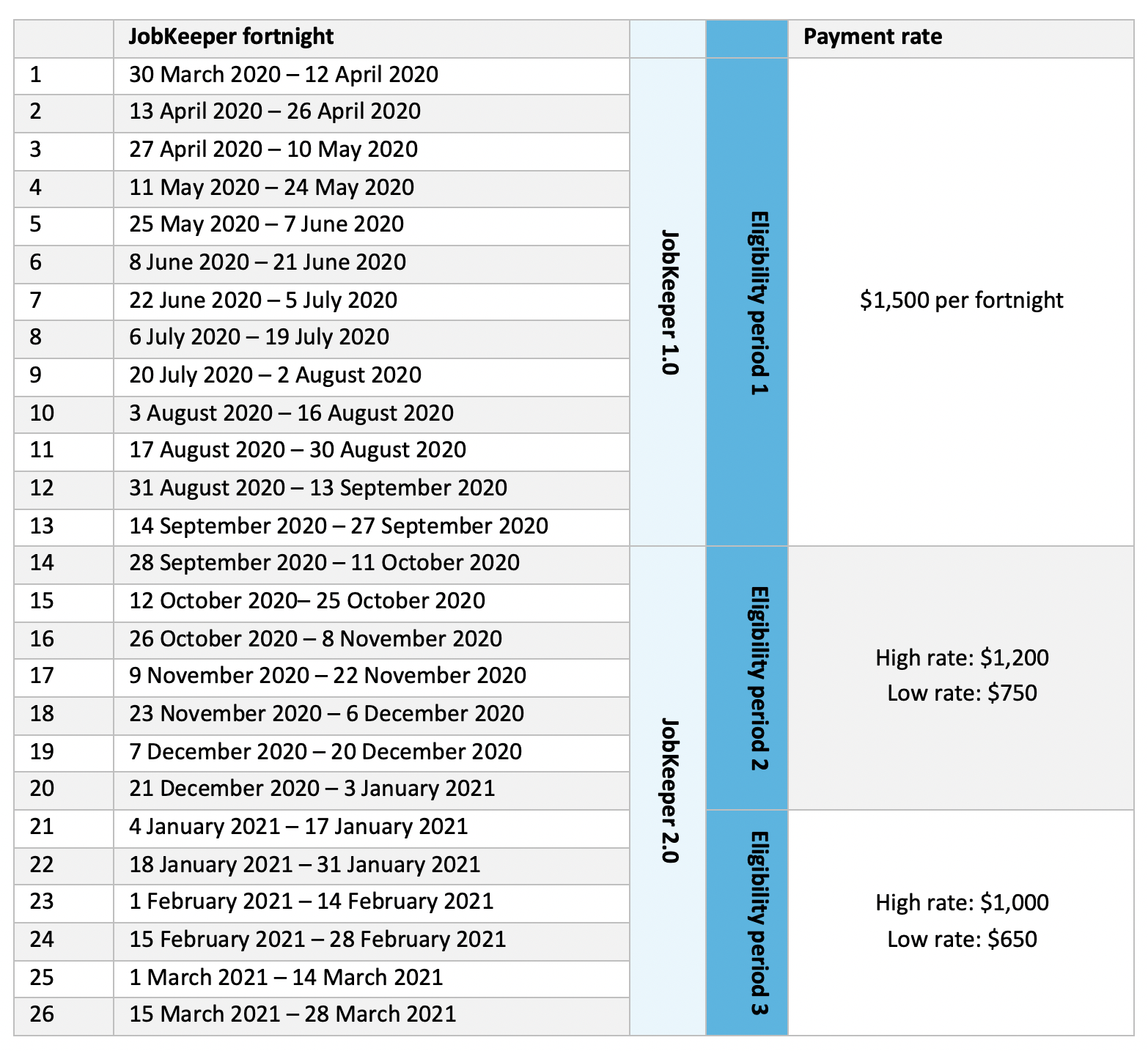

From 28 September 2020, the eligibility tests to access JobKeeper for employers will change, as will the amount of the JobKeeper payment for employees and business participants. To receive JobKeeper from 4 January 2021, employers will need to assess their eligibility again.

Eligibility for one JobKeeper period does not entitle you to, or exclude you from, payments in another period. Each eligibility period is addressed separately. That is, there might be businesses that qualified for the first tranche of JobKeeper, don’t qualify for the second tranche but qualify for the third.

1. Eligible businesses

Eligible employers

An eligible employer is an employer that:

- On 1 March 2020, carried on a business in Australia or was a non‑profit body pursuing its objectives principally in Australia; and

- before the end of the JobKeeper fortnight, it met the original decline in turnover test*:

- And, was not:

- on 1 March 2020, subject to Major Bank Levy for any quarter ending before this date, a member of a consolidated group and another member of the group had been subject to the levy; or

- a government body of a particular kind, or a wholly-owned entity of such a body; or

- at any time in the fortnight, a provisional liquidator or liquidator has been appointed to the business or a trustee in bankruptcy had been appointed to the individual’s property.

1 March 2020 is an absolute date. An employer that had ceased trading before 1 March, commenced after 1 March 2020, or was not pursuing its objectives in Australia at that date, is not eligible.

*Additional tests apply from 28 September 2020.

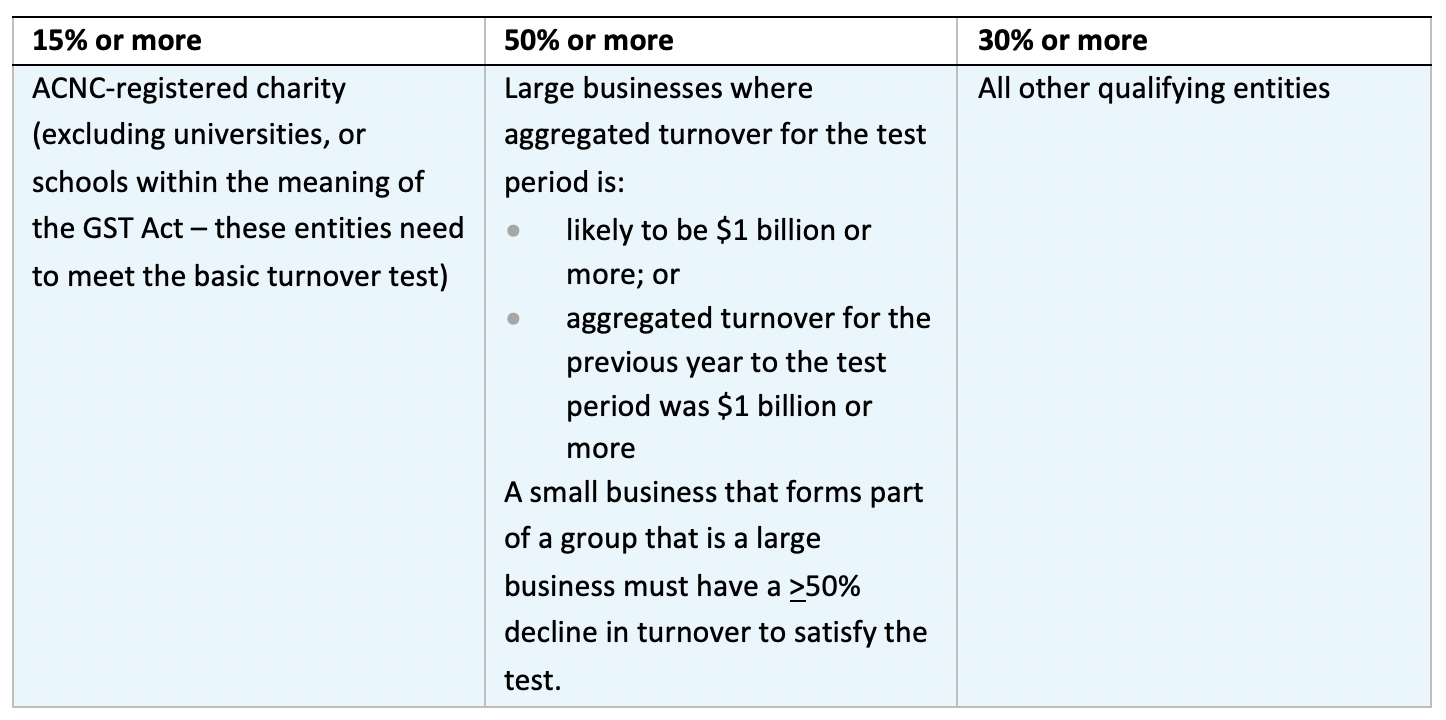

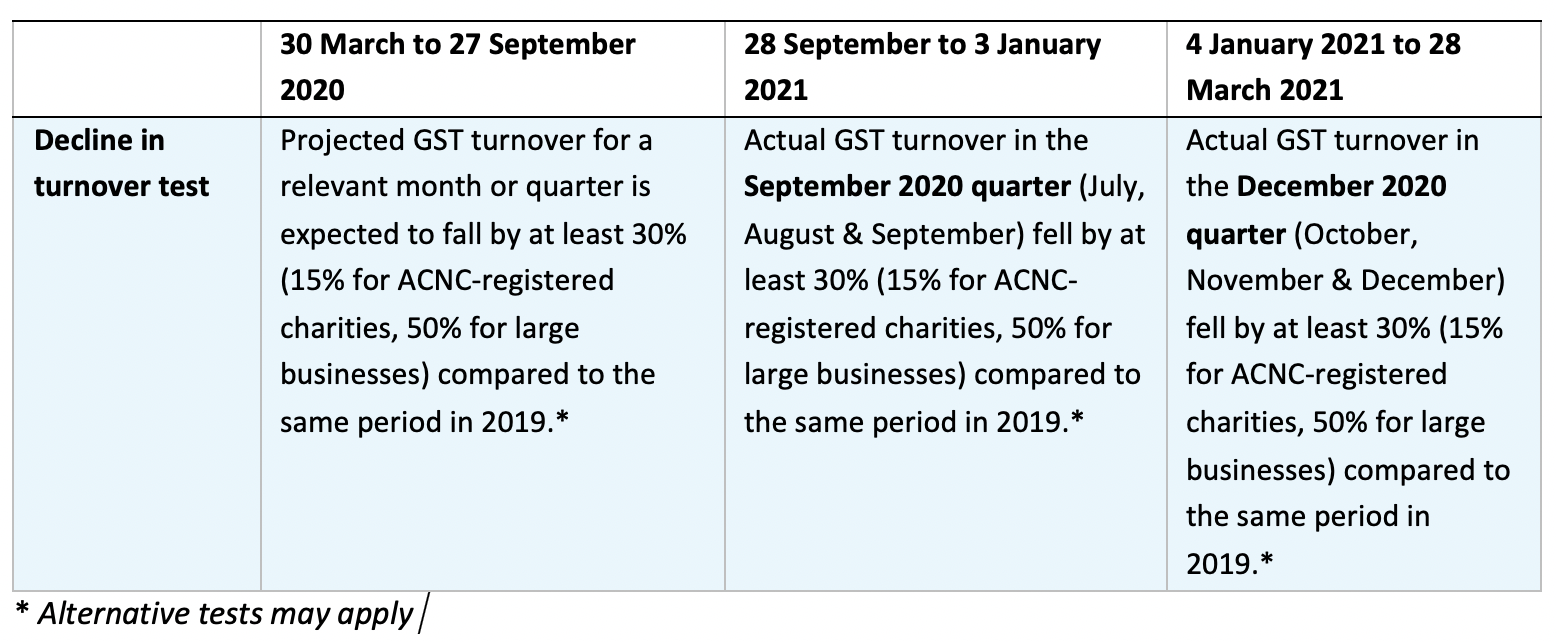

The decline in turnover test

For businesses already enrolled in JobKeeper, to receive payments from 28 September 2020, you need to meet an extended decline in turnover test based on actual GST turnover.

Businesses that are enrolling for the first time, need to meet the basic eligibility test and the decline in turnover test/s for the relevant period.

Most businesses will generally use their Business Activity Statement (BAS) reporting to assess eligibility. However, as the BAS deadlines are generally not until the month after the end of the quarter, eligibility for JobKeeper will need to be assessed in advance of the BAS reporting deadlines to meet the wage condition for eligible employees.

Calculating GST turnover

Calculating GST turnover for tranches 2 and 3 of JobKeeper is different to the original JobKeeper requirements as entities will only be using current GST turnover figures (not projected GST turnover).

When applying the new turnover reduction tests for the September 2020 quarter and December 2020 quarter, entities that are registered for GST must use the same method that is used for GST reporting purposes. That is, if the entity is registered for GST on a cash basis then a cash basis needs to be used to calculate current GST turnover for the purpose of these new tests

Current GST turnover includes proceeds from the sale of capital assets, unless the sale is input taxed. Current GST turnover includes taxable and GST-free supplies, but should exclude input taxed supplies such as residential rental income and financial supplies like dividends, interest etc. JobKeeper and ATO cash flow boost payments should be excluded from the calculation along with other payments that don’t represent consideration for a supply made by the entity such as certain State based grants.

2. Eligible employees

From 3 August 2020, the eligibility tests for employees were changed to enable a greater number of employees to access JobKeeper.

Previously, an employee had to be employed by the relevant entity on 1 March 2020 to be eligible for JobKeeper payments. Someone employed as a casual on that date also must have been employed on a regular and systematic basis for the 12 month period leading up to 1 March 2020.

Now, employees who were previously ineligible for JobKeeper because they were not employed by the entity on 1 March 2020 may be able to receive JobKeeper payments if they were employed by the entity on 1 July 2020 and can fulfil all of the other eligibility requirements. If an employee already passed all the relevant conditions at 1 March 2020 then they don’t need to be retested using the 1 July 2020 test date.

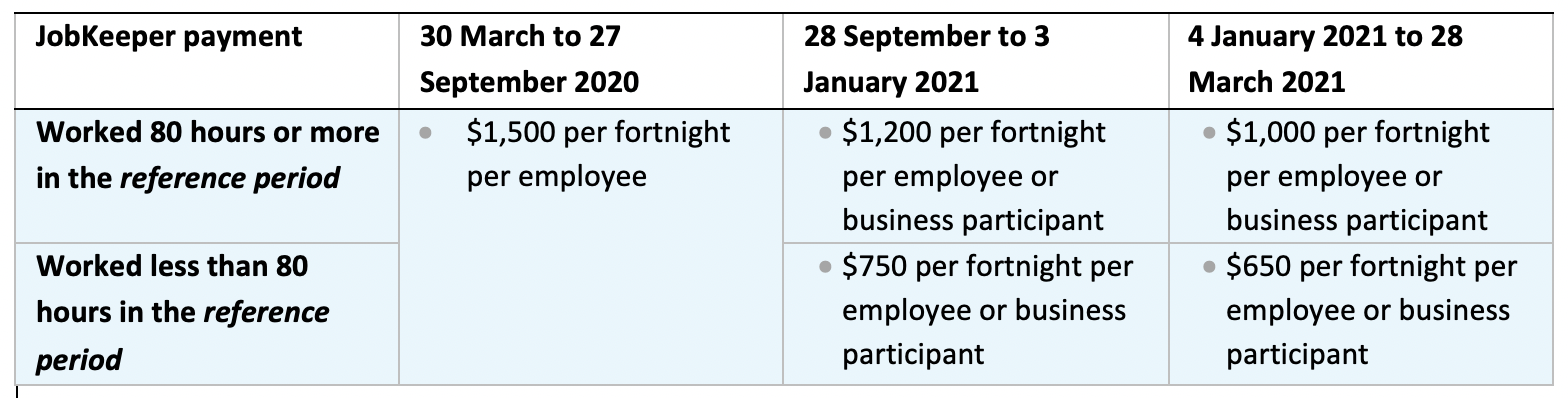

3. JobKeeper payments

From 28 September 2020, the payment rate for JobKeeper will taper from the flat rate of $1,500 and split into a higher and lower rate.

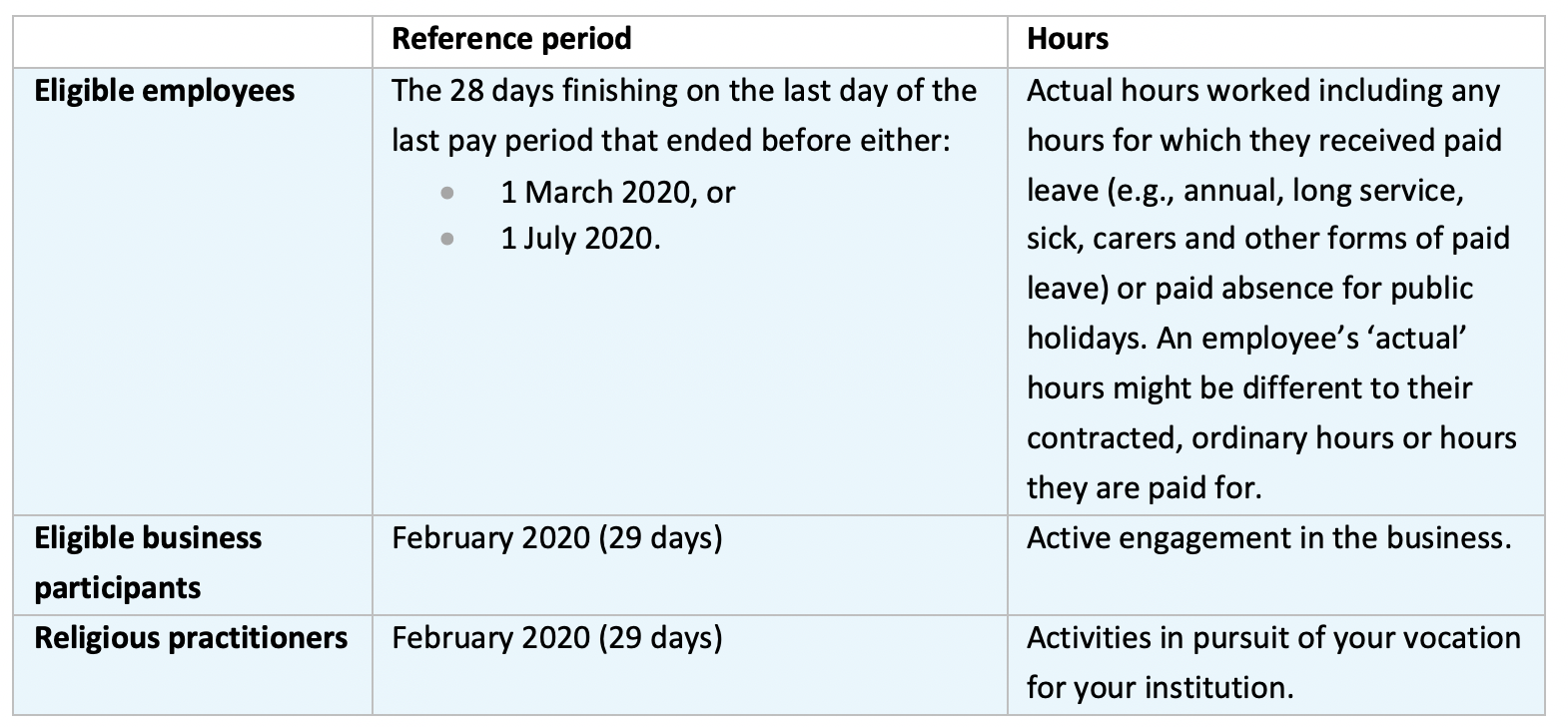

What’s a reference period?

JobKeeper fortnights

.svg)

.svg "page-1 (4)")